Carbon Capture Coalition Welcomes IRS Issuance of Proposed 45Q Rule and Requirements for Secure Geologic Storage

May 29, 2020 | News

Carbon Capture Coalition Director Brad Crabtree has released the following statement regarding the Treasury Department and Internal Revenue Service issuance of proposed regulations to implement the Section 45Q tax credit:

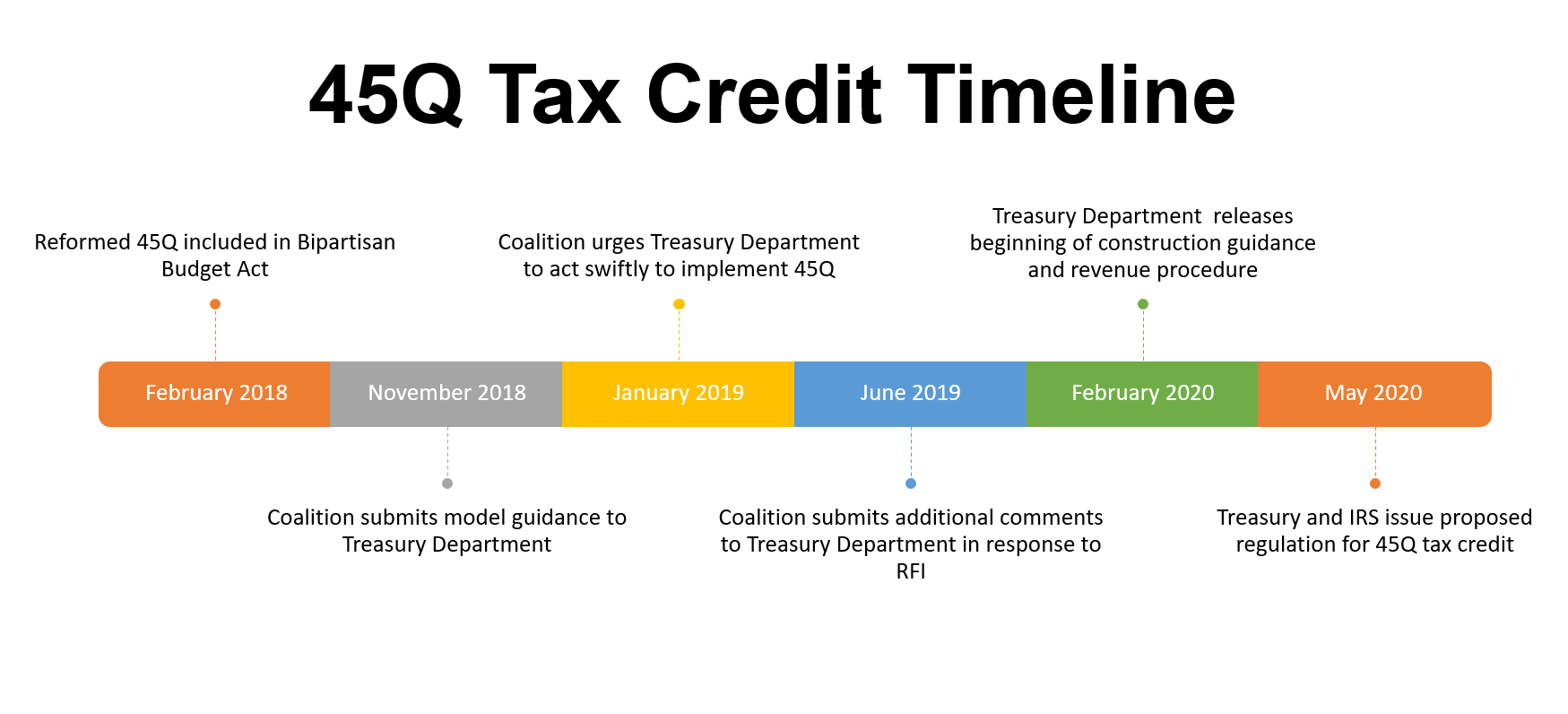

“The Carbon Capture Coalition is pleased that the Treasury Department and IRS have released proposed regulations addressing remaining long-term issues associated with implementation of the reformed 45Q tax credit, which was signed into law in early 2018. The Coalition commends the IRS for its comprehensive and thorough approach and for being responsive to its recommendations.

With the release of this proposed rule, developers and investors now have the remaining critical information they need to continue moving forward on roughly 30 identified commercial carbon capture projects already under development nationwide in response to the revamped 45Q credit.

The Coalition particularly welcomes the IRS’ proposed requirements for demonstrating secure geologic storage. Importantly, the IRS explicitly rejected recommendations from some parties that would have relaxed existing robust monitoring, reporting and verification (MRV) requirements for demonstrating geologic storage and risked undermining policymaker and public faith in the 45Q program.

The Coalition’s over 75 companies, NGOs and unions worked together for months to develop consensus recommendations calling on the IRS to: 1) affirm the existing MRV pathway to claim the 45Q tax credit under EPA’s Subpart RR rule of the federal Greenhouse Gas Reporting Program; and 2) provide for an additional and equivalent MRV program, based on the recently-approved ISO standard for geologic storage of carbon dioxide (CO2) and supplemented with public transparency and accountability provisions.

In addition to reaffirming Subpart RR as an approved method in its beginning construction guidance released in February, the IRS has also now provided for an additional ISO-based pathway in the proposed rule.

The IRS also explicitly agrees with the Coalition and others who have long advocated for increased transparency in public reporting, but it cites a lack of statutory authority to require it. The Coalition will now consider existing IRS authorities and determine whether to recommend that Congress give the IRS additional legislative authority to bring more public sunlight into the process of companies demonstrating that they have met the requirements of the tax credit. Enhanced transparency, together with the IRS’ rigorous ongoing auditing and enforcement revealed in the recent IRS Inspector General’s report, should provide for public confidence in the reformed and expanded 45Q program going forward.

The proposed rule also addresses in detail other key priorities identified by the Coalition in its recommendations, including credit recapture, transferability of the credit and contractual assurance, and the lifecycle analysis requirement to claim the 45Q credit for emission reductions achieved through the use of captured carbon in manufacturing low and zero-carbon fuels, chemicals, materials and other products.

Coalition participants will carefully evaluate what the IRS has proposed in the proposed regulation and the Coalition’s priority areas and provide formal consensus comments in response within the 60-day comment period.

Following this long-overdue release of the proposed 45Q rule, it is time for Congress to act immediately to avoid further delays to carbon capture projects that must begin construction by the end of 2023 to qualify for the 45Q tax credit. Project developers now face an aggressive and rapidly closing window to plan, engineer, permit and finance potential projects amidst an unprecedented economic crisis caused by the COVID-19 pandemic that has constrained tax equity markets, a major source of needed private investment.

Therefore, the Carbon Capture Coalition once again calls on Congress to advance its top two legislative priorities—enacting a multiyear extension of 45Q, coupled with the option of direct pay to provide a cash payment in lieu of the tax credit—to enable developers to finance and continue their projects, sustaining urgently needed economic activity and jobs at a time of national crisis.”

To read more about the Coalition comments submitted to Treasury and the IRS on 45Q, read the June 28, 2019 press release on our website.

Share this post