Brad Crabtree Testifies Before US House Select Committee on the Climate Crisis

September 26, 2019 | Legislation

Great Plains Institute Vice President Brad Crabtree was asked to testify before the House Select Committee on the Climate Crisis in his role as director of the Carbon Capture Coalition. He spoke at the hearing, “Solving the Climate Crisis: Reducing Industrial Emissions Through US Innovation,” about the critical need for economywide deployment of carbon capture to reduce industrial carbon emissions at scale.

As Brad describes in his testimony, leading analysis shows that carbon capture is needed to reach emissions reduction targets by 2050. Industrial emissions account for about one-third of global carbon emissions and those emissions are growing at twice the rate of emissions as a whole.

Carbon capture is essential to achieve emissions reductions in industries that are otherwise difficult to decarbonize, and can enable them to create products of economic value and lower carbon intensity, from steel to concrete, that can sustain and create high-paying jobs. Brad’s testimony lays out a portfolio of federal incentives and other policies released earlier this year by the Carbon Capture Coalition that will support economywide deployment of carbon capture and help put the US on a path toward midcentury decarbonization.

Brad’s written testimony from the House Select Committee on the Climate Crisis is available below and video of the hearing is available on YouTube. (Brad’s remarks are at 34:15) Additionally, the committee had a number of follow up questions, which Brad answered and submitted for the record. You can read those responses here.

Testimony of Brad Crabtree to the House Select Committee on the Climate Crisis

September 26, 2019

Chairwoman Castor, Ranking Member Graves, and Members of the Select Committee, thank you for inviting me to testify. My name is Brad Crabtree, and I am vice president for Carbon Management at the Great Plains Institute. I am here today in my capacity as director of the Carbon Capture Coalition, a national partnership of over 70 energy, industrial and technology companies, labor unions, and environmental, clean energy and agricultural organizations.

My testimony will address:

• the essential role that carbon capture must play in managing industrial carbon emissions to meet midcentury climate goals;

• existing examples of US and global technology innovation and leadership; and

• key elements of a US federal policy framework needed to achieve deployment of carbon capture technologies in key carbon-intensive industrial sectors.

Carbon Capture is Essential to Managing Industrial Emissions to Meet Midcentury Climate Goals

The Carbon Capture Coalition was established in 2011 to help realize the full potential of carbon capture as a national strategy for reducing carbon emissions, supporting domestic energy and industrial production, and protecting and creating high-wage jobs. The Coalition’s members have forged an alliance of unprecedented diversity in the context of U.S. federal energy and climate policy, and they are dedicated to achieving a common goal: economywide deployment of carbon capture from industrial facilities, power plants, and ambient air.

Economywide deployment of carbon capture is indispensable to reducing industrial emissions. In March, the Coalition’s industry, labor and NGO participants submitted a joint letter to this Committee and other committees of jurisdiction urging Congress “to include carbon capture research, development, and commercial deployment as an essential component of a broader strategy to decarbonize power generation and key industry sectors by midcentury.”

In their letter, Coalition participants pointed to modeling by the International Energy Agency (IEA) and the Intergovernmental Panel on Climate Change (IPCC) that illustrates the critical role carbon capture must play in industrial decarbonization to meet climate goals. For example, in its modeling of scenarios for limiting warming to 2° Celsius, the IEA found that carbon capture must contribute 14 percent of cumulative emissions reductions by midcentury and 20 percent annually by 2050, with 45 percent of those reductions coming from industrial sources.

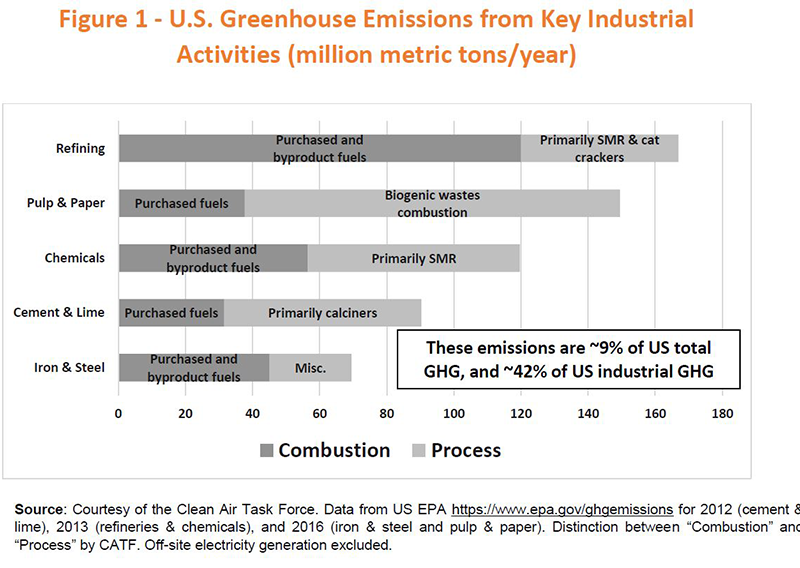

Capture from industrial facilities is not optional from a climate perspective. Industrial sources constitute roughly one third of global and domestic carbon emissions. While a range of measures can be taken to decarbonize energy inputs into industrial production (including carbon capture in power generation and reforming natural gas to produce hydrogen), many sources of carbon emissions are inherent to the chemistry of industrial processes themselves, which often have few, if any, alternative mitigation options available beyond carbon capture. Figure 1 highlights the significance of process emissions as a component of broader industrial emissions from refining, pulp and paper, chemicals, cement and lime, and iron and steel production.

The outputs of these and other industries are central to modern life, underpinning the livelihoods of millions of Americans and contribute to the economic and social stability of entire communities and regions across our nation. Industrial production and associated energy production and manufacturing support a high-skill, high-wage jobs base, yet these sectors’ low-margin, trade-exposed commodity businesses leave them vulnerable to increases in costs incurred to reduce emissions. Deployment of carbon capture technologies, coupled with appropriate financial incentives and other policies to reduce costs and buy down risk, can enable the decarbonization and continued operation of existing industrial facilities, while avoiding their closure and the offshoring of jobs and livelihoods.

US and global technology innovation and leadership

To underscore the challenge before us, over half of global industrial carbon emissions come from just three sectors—steel, cement and basic chemicals—and over half of those three industries’ emissions are process emissions unrelated to energy inputs. Yet, there is only one large-scale commercial carbon capture facility operating in the world today in these three industries, and that is a steel plant in the United Arab Emirates.

Fortunately, carbon capture works, and we have a strong foundation of American technology leadership on which to build as we embark on strategies and policies to reduce industrial carbon emissions while sustaining our country’s high-wage jobs base. Currently, there are 23 large-scale carbon capture and storage facilities operating in the world today, capturing nearly 40 million metric tons of CO2 annually. Ten of those large-scale facilities are located in the U.S. In terms of industrial carbon capture, there are 12 operating commercial-scale facilities in the U.S. that capture CO2 from a variety of industrial sources. They have a combined annual capture capacity of just over 25 million metric tons. The transport, use and geologic storage of that CO2 is enabled by roughly 5,000 miles of existing CO2 pipelines in 11 states.

Successful commercial and operational experience with large-scale industrial carbon capture with geologic storage dates back to 1972 in the US, when oil companies in West Texas first began capturing CO2 from natural gas processing for use in enhanced oil recovery. Next, industrial carbon capture expanded to gasification for fertilizer and substitute natural gas production, followed by capture from fermentation at ethanol plants. Finally, large-scale commercial carbon capture from refinery hydrogen production came on line earlier in this decade.

These successful examples of commercial carbon capture represent higher purity industrial sources of CO2 with lower costs of capture. These “low-hanging fruit” for industrial decarbonization include fermentation in ethanol production, gas processing, gasification and natural gas reformation for hydrogen production, all of which produce relatively pure streams of CO2. Their costs of CO2 capture and compression are now within range of the newly revamped federal Section 45Q tax credit. A key remaining deployment need for these sectors is federal support for financing additional infrastructure to transport the CO2 from where it is captured to where it can be stored or put to beneficial use.

A second tier of industrial processes produce lower-purity streams of CO2, and these include cement, catalytic cracking in refining, and steel production. These lower purity sources have seen little or no commercial-scale deployment of capture technology because of their higher capture costs. To varying degrees, they will need additional federal policy support for early commercial demonstration to complement the existing 45Q tax credit to reach financial feasibility.

In addition to effective demonstration of capture technologies, commercial markets and uses of captured industrial CO2 in the U.S. have expanded over time as well. Until this decade, most CO2 captured from industrial sources was utilized and geologically stored through enhanced oil recovery, with some CO2 destined for food and beverage, dry ice and other high-value niche markets. In 2017, Archer Daniels Midland began large-scale storage of CO2 from ethanol production in a saline geologic formation, a geologic storage pathway anticipated to grow significantly now that the 45Q tax credit provides $50 per metric ton for saline storage over $35 per ton for CO2 stored through EOR. Looking ahead, rapidly growing interest and investment in the development and commercialization of different technology pathways to produce fuels, chemicals, building products, advanced materials and other beneficial products from captured carbon will create new markets for industrial emissions of carbon dioxide and its precursor carbon monoxide. To build upon the well-established pathway of CO2 use and geologic storage through CO2-enhanced oil recovery, it is critical that federal policy prioritize further development and commercial deployment of large-scale saline geologic storage and creation of new markets for captured carbon through stepped up R&D into beneficial uses of both CO2 and CO.

American industry, labor and NGO leaders and federal and state officials are also learning from technology innovation overseas for application here at home. Earlier this month, a U.S. delegation coordinated by the Great Plains Institute traveled to the United Arab Emirates, where Emirates Steel began capturing 800,000 metric tons annually of CO2 since 2016, and to Belgium, where ArcelorMittal is partnering with U.S. technology firm LanzaTech to construct a facility that will use microbes to transform waste carbon monoxide emissions captured from steel production into 17.5 million gallons of ethanol annually.

These successful examples of industrial carbon capture, coupled with emerging innovation in carbon utilization technologies and business models, are spurring the interest of U.S. companies, entrepreneurs and investors in a circular industrial economy in which waste carbon dioxide and carbon monoxide emissions become a source of economic value and part of the climate solution.

A robust federal policy framework is needed to sustain U.S. leadership and achieve economy-wide deployment of carbon capture in key carbon-intensive industrial sectors

Federal policy has a critical role to play in helping to sustain American leadership and innovation in building this new carbon economy. Congress is to be commended for bipartisan passage last year of the FUTURE Act, a landmark reform and expansion of the Section 45Q tax credit for geologic storage and beneficial use of carbon captured from industrial facilities, power plants and ambient air.

To build on this cornerstone federal policy, the Carbon Capture Coalition released a Federal Policy Blueprint to Congress earlier this year, recommending federal financial incentives and other policies to complement the 45Q credit in driving private investment, and spurring innovation and cost reductions sufficient to achieve economywide deployment of carbon capture. The Coalition defines economywide deployment as advancing a critical mass of commercial-scale projects in key industrial sectors and power generation between now and 2030 to enable the scaling of the technology by midcentury to reach decarbonization goals. It’s worth noting that the Blueprint reflects a consensus of the over 70 companies, unions and NGOs participating in the Coalition—a rarity on matters of federal energy, industrial and climate policy.

In crafting the Blueprint, Coalition participants recognized that an array of federal policies have supported the development and commercial scale-up of wind, solar and other low and zero-carbon technologies in the marketplace and that economywide deployment of carbon capture will require a comparable portfolio of policies. Toward that end, the Coalition recommends a package of federal policies that spans the full value chain of carbon capture, transport, use, removal and geologic storage.

The Carbon Capture Coalition’s strategic vision for future policy action is to:

• Ensure effective implementation of 45Q by the U.S. Treasury to provide the investment certainty and business model flexibility intended by Congress;

• Provide additional federal incentives to complement, expand and build upon 45Q in financing carbon capture, utilization, removal and storage projects;

• Incorporate carbon capture, transport, utilization, removal and storage into broader national infrastructure policy; and

• Expand, retool and prioritize federal funding for research, development, demonstration and deployment (RDD&D) of the next generation of carbon capture, utilization, removal and geologic storage technologies and practices.

Economywide deployment of carbon capture will require federal legislative and administrative action in the following areas:

Investment Certainty

Effective implementation of the 45Q tax credit is crucial to providing the financial certainty and flexibility needed to leverage the private investment in projects sought by Congress. In particular, a longer time horizon for federal policy is needed to support early commercial-scale demonstrations of essential carbon capture technology in the most carbon-intensive industrial sectors, given long lead times needed to develop, permit, finance and construct such projects. The Coalition welcomes recent signals from the Treasury Department that the Internal Revenue Service (IRS) is now prioritizing completion of guidance to implement the 45Q tax credit, but significant concerns remain that hundreds of millions and perhaps billions of dollars in private capital remain on the sidelines as project developers and investors have waited 19 months for clarity from Treasury and the IRS.

Key Policy Priorities

• Lawmakers should extend the commence construction window for 45Q beyond the end of 2023 given Treasury delays on guidance and to send a signal of long-term policy continuity to project developers and investors.

• IRS should provide an additional equivalent pathway for demonstrating secure geologic storage through CO2-EOR (in addition to the existing federal Subpart RR Greenhouse Gas Reporting Program) based on the International Organization for Standardization (ISO) Standard 27916 and supplemented with additional public transparency and accountability measures as recommended in the Coalition’s June 28, 2019 comments to Treasury.

• Facilitate CO2 transport infrastructure planning, siting and permitting through passage of the USE IT Act to help ensure the availability of infrastructure needed for development of carbon capture, use and geologic storage projects.

Technology Deployment & Cost Reductions

Just as federal investments in research, development, demonstration and deployment (RDD&D) have successfully helped scale up wind, solar and other low and zero-carbon energy technologies in the marketplace, expanding, retooling and prioritizing federal investments in transformational carbon capture, utilization, storage and removal technologies will be a critical component of driving down costs of carbon capture and utilization in key industrial sectors and making sure that the next generation of technologies with reduced costs and increased performance make their way to the marketplace. In this context, it is especially crucial that an expanded federal RDD&D program prioritize later-stage demonstrations of critical industrial capture and utilization technologies and not just early stage research and development.

The Carbon Capture Coalition welcomes and supports the many current bipartisan legislative efforts to update and expand federal authorities and funding for industrial carbon capture, utilization and storage as part of a broader innovation agenda. These bills enjoy widespread bipartisan and bicameral support and should be passed this Congress.

Key Policy Priorities

• Ensure robust federal appropriations for carbon capture, utilization, removal and storage RDD&D, ensuring inclusion of diverse industry sectors and processes, technology pathways and energy resources.

• Retool and expand federal RDD&D programs, including near-term passage of bipartisan legislation such as the USE IT Act, House Fossil Energy R&D Act, Senate EFFECT and LEADING Acts, and Clean Industrial Technology Act.

• Provide DOE cost share for Front-End Engineering and Design (FEED) studies to support the development of critical, commercial-scale industrial carbon capture and utilization and other technology demonstration projects.

Project Finance & Feasibility

An expanded portfolio of incentive policies to enhance and expand upon the 45Q tax credit will ultimately be necessary to foster early stage commercial demonstration and broader economywide deployment of industrial carbon capture and utilization technologies. These include: improvements to 45Q and other existing tax incentives that enhance monetization; technical corrections to 45Q that broaden eligibility and access; and complementary policies that contribute to overall financial feasibility by lowering the cost of debt and equity, reducing commodity risk and expanding markets.

An expanded incentive portfolio will be especially important to achieve widespread demonstration and deployment of carbon capture in three areas of crucial importance to industrial decarbonization: carbon-intensive industrial processes with higher costs of capture, such as the manufacture of steel and cement; electric generation needed to power and, where feasible, further electrify industrial processes; and natural gas reformation with carbon capture, which currently offers the lowest-cost pathway to provide zero-carbon hydrogen for process heat and other industrial applications.

Given the significant role that the federal government plays in the purchase of cement, steel and other key industrial commodities, federal procurement policy will play an especially important part in building markets for early commercial carbon capture and utilization projects in industry. In the case of low-margin industrial commodities, federal procurement policy can enable early innovators and investors to deploy technology to deliver a low or zero-carbon product to market, while only adding marginally to the total cost of federally-funded infrastructure, buildings and other projects.

Key Policy Priorities

Monetizing Financial Incentives

• Prevent the disallowance of 45Q under the BEAT Tax, similar to treatment of the Production Tax Credit for wind and Investment Tax Credit for solar.

• Enhance transferability of the 45Q tax credit consistent with the 45J tax credit for advanced nuclear.

• Provide a revenue-neutral refundability option for 45Q.

• Establish a 45Q bonding mechanism.

Technical Corrections to Expand Eligibility and Access

• Eliminate the 25,000-ton annual capture threshold in 45Q for carbon utilization projects.

• Fix the 48A tax credit to enable carbon capture retrofits of existing power plants (Carbon Capture Modernization Act).

Federal Policies to Complement 45Q

• Make carbon capture projects eligible for tax-exempt private activity bonds (Carbon Capture Improvement Act).

• Provide for eligibility of carbon capture projects for tax-advantaged master limited partnerships (Financing Our Energy Future Act).

• Reform the DOE Loan Program.

Creating Predictable Markets for Carbon Capture and Utilization

• Develop federal procurement policies for electricity, fuels and products produced from carbon capture, utilization, removal and geologic storage.

• Reduce commodity risk through federal contracts-for-differences (CfDs).

• Incentivize commercial production of low-carbon fuels from captured carbon.

• Ensure eligibility for carbon capture, if Congress enacts a federal electricity portfolio standard.

• Provide an enhanced investment tax credit for transformational carbon capture technologies.

Infrastructure Deployment

To achieve the full potential of carbon capture to reduce industrial emissions, while protecting and creating high-wage jobs, we must responsibly scale up infrastructure to create a nationwide network for transporting CO2 captured from industrial facilities, power plants and ambient air to locations around the country where it can be put to beneficial use or safely and permanently stored in geologic formations. This buildout will include capacity expansions and extensions of existing pipeline networks, as well as the construction of long-distance, large-volume interstate trunk lines to serve states and regions that currently lack such infrastructure.

Key Policy Priorities

• Provide low and zero-interest federal loans to supplement private capital in financing pipeline projects.

• Provide federal grants to cover the incremental cost of supersizing pipelines to provide for extra capacity and realize economies of scale.

• Support flagship demonstration projects in key regions of the country, featuring large-volume, long-distance interstate trunk lines linking multiple industrial facilities and power plants that supply CO2 to multiple utilization and geologic storage sites.

• Facilitate planning, siting and permitting of CO2 transport infrastructure (USE IT Act).

• Provide eligibility for tax-exempt private activity bonds and master limited partnerships (Carbon Capture Improvement Act and Financing our Energy Future Act, respectively).

In summary, economywide deployment of carbon capture, use and geologic storage is not optional if we are to decarbonize industry and achieve midcentury climate goals. Carbon capture technology provides a viable pathway to enable the decarbonization and continued operation of existing and new industrial facilities, while avoiding plant closures and the offshoring of jobs and livelihoods. The US is the world’s leader in the capture, use and geologic storage of CO2 from industry, with nearly 50 years of successful commercial and operational experience on which to build. We now have an opportunity to enact a broader portfolio of federal incentives and other policies for carbon capture, transport, use, removal and geologic storage. We must learn from our successful experience with wind, solar and other low and zero-carbon technologies and implement a broader policy framework for carbon capture in order to sustain US leadership and help put our nation on a path toward midcentury decarbonization.

Thank you again for your opportunity to testify, and I look forward to your questions.

Share this post